SAVINGS, SOURCE FOR LENDING – EXPECT INCOME TAX EXEMPTION

MANY OF THE ‘MIDDLCE CLASS’ INDIANS HAVE THE HABIT OF SAVINGS TO MEET THEIR, SUCCESSORS’ FUTURE NEEDS, SINCE WE ARE LIVING UNDER UNSECURE FUTURE CIRCUMSTANCES. THEY WOULD LIKE TO KEEP THEIR SAVINGS IN LIQUID FORM OF CASH, RISK FREE DEPOSITS WITH POSTAL DEPARTMENT, BANKS, FINANCIAL INSITUTIONS SO THAT THEY CAN MEET THEIR NEEDS ON TIME […]

Read More

SAVINGS, SOURCE FOR LENDING – EXPECT INCOME TAX EXEMPTION

MANY OF THE ‘MIDDLCE CLASS’ INDIANS HAVE THE HABIT OF SAVINGS TO MEET THEIR, SUCCESSORS’ FUTURE NEEDS, SINCE WE ARE LIVING UNDER UNSECURE FUTURE CIRCUMSTANCES. THEY WOULD LIKE TO KEEP THEIR SAVINGS IN LIQUID FORM OF CASH, RISK FREE DEPOSITS WITH POSTAL DEPARTMENT, BANKS, FINANCIAL INSITUTIONS SO THAT THEY CAN MEET THEIR NEEDS ON TIME […]

Read MoreISSUE WITH REGARDING PROPOSED COMPANY LAW

I am herewith presenting some of my personal views to be discussed with regarding the proposed Company Law. I. COMPANY LAW The Proposed Company Law has to consider the following issues: FACE VALUE OF SHARES: There should be uniformity face value of forms @ Rs.10/- each and should not have any other face values so […]

Read More

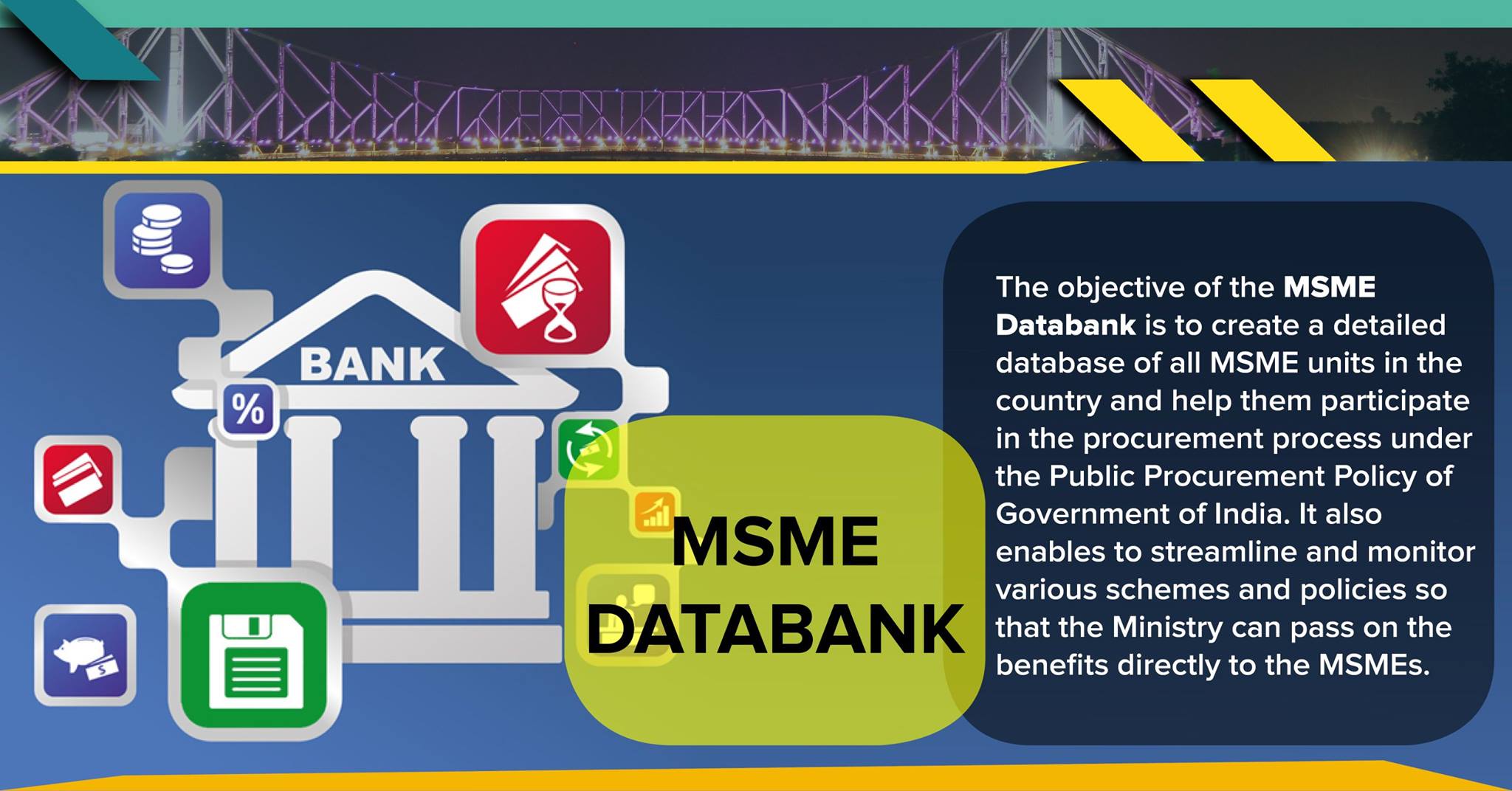

BANKS – MSME UNITS – NPA ISSUES

AT PRESENT BANKS ARE FACING RECOVERY PROBLEMS OF LOANS ISSUED. THE REASONS MAY BE DUE TO LOANS GI VEN TO MANUFACTURING TRADING REVENUE BASESD PROJECTS PERSONAL, HOUSING, VEIHCLES OTHERS. REASONF FOR DEFAULT LONGE PROCESS PERIOD, MORE STOCKS, RECEIVABLES EASY TO SELL, LACK OF MARKET LONGER OERFIRNABCE PERIOD, EXPECTATIONS MAY VARY OWN PERSONAL ARRANGMENT, SOURCES […]

Read MoreExpenditure Allowable as Deduction (Section 36)

*** *** ALLOW ABILITY OF EXPENDITURE (SECTION 37) 1. Conditions for allow ability of expenditure: There should be an expenditure of revenue nature incurred during the previous year. The expenditure should not be Capital in nature. It should be incurred in connection with business or profession carried on by the assessee. It should have been […]

Read MoreAllow ability of Expenditure incurred for Scientific Research (Section 35)

All 1. Expenditure on in-house research: The following expenditure incurred by the assessee on scientific research in relation to the assessee’s business shall be allowed as deduction- Current year expenditure: Current year revenue expenditure or Capital expenditure on scientific research. Prior period expenditure: Prior period revenue expenditure or capital expenditure incurred during 3years immediately preceding […]

Read MoreAvailability of Deduction to the Assessee engaged in the business of growing and manufacturing Tea or Coffee or Rubber in India (Section 33AB)

1. Applicability: All assesses who carry on the business of growing and manufacturing tea or coffee or rubber in India. 2. Pre-condition: The assessee should deposit the amount in NABARD or special Deposit Account within earlier of 6months from the end of the relevant previous year or before the due date of filing return of […]

Read MoreALLOWABILITY OF EXPENDITURE INCURRED FOR SCIENTIFIC RESEARCH (SECTION 35)

1. Expenditure on in-house research: The following expenditure incurred by the assessee on scientific research in relation to the assessee’s business shall be allowed as deduction- Current year expenditure: Current year revenue expenditure or Capital expenditure on scientific research. Prior period expenditure: Prior period revenue expenditure or capital expenditure incurred during 3years immediately preceding the […]

Read MoreConditions regarding allow ability of interest on partner’s capital (Sec.40 (b))

1. Conditions: The payment should be authorized by the partnership deed. It should be for the period falling after the date of partnership deed. 2. Exception: The above condition does not apply in the following situations- Where an individual is a partner on behalf of or for the benefit of any other person, and interest […]

Read More